Business Model

Is Arista Networks a great business? Arista Networks is a business that reflects solid business fundamentals and consistent revenue and operating income growth since it became a public company in June 2014. It is therefore worth taking a further look into this business. Simple business models with a long track record are more predictable and less likely to be subject to disruption. Arista does not operate a simple and predictable business. It is a networking equipment provider. Arista Networks is an industry leader in data-driven, client-to-cloud networking for large AI, data center, campus and routing environments. Its award-winning platforms deliver availability, agility, automation, analytics, and security through an advanced network operating stack.

Arista was founded by industry luminaries Andy Bechtolsheim, Ken Duda and David Cheriton, launched in 2008 and is led by CEO Jayshree Ullal. Its seasoned leadership team is globally recognized as respected leaders and visionaries with a rich and extensive history in networking and innovation. The company went public in June 2014, is listed with NYSE (ANET), and currently has over 8,000 cloud customers worldwide. Arista Networks (ANET) is a networking equipment provider that primarily sells Ethernet switches and software to data centers. Its marquee product is its extensible operating system, or EOS, that runs a single image across every single one of its devices. The firm operates as one reportable segment. It has steadily gained market share since its founding in 2004, with a focus on high-speed applications. Arista counts Microsoft and Meta Platforms as its largest customers and derives roughly three quarters of its sales from North America. Specifically, Meta and Microsoft accounted for 21% and 18% of Arista’s revenue in 2023, respectively. This means these two companies alone contributed almost 40% of total revenue. As a technology hardware provider, this is not a simple business. This business is subject to competition and the risk that other companies can produce more advanced and superior technology therefore its future is less predictable.

Market Position

Arista does not have a dominant market position in its industry. However, Arista Networks has been steadily increasing its market share in the Ethernet switch market, particularly in the datacenter segment. As of 2024, Cisco Systems is still the dominant player, but its share is gradually declining. The other competitors are Juniper Networks and Extreme Networks. Overall,Arista holds a respectable market share in the Ethernet Switch Market, though significantly smaller than Cisco’s. Recent data suggests they’re hovering around 10% of the overall market. Arista’s strength lies in the datacenter segment where they have a larger share due to their focus on high-speed Ethernet switches and cloud data centers. They’ve been gaining ground in this segment. Arista’s strong position in the datacenter segment is crucial, as this area is experiencing significant growth with the rise of cloud computing and AI.

High Return on Invested Capital

One important criteria of a great business is that the company should efficiently allocate capital and generate high returns on its capital. Charlie Munger famously said,

“Over the long term it is hard for a stock to earn a much better return than the business that underlies its earnings… If a business earns 6% on capital over 40 years and you hold it for that 40 years, you’re not going to make much different than a 6% return – even if you originally buy it at a huge discount”

Munger’s statement highlights the importance of investing in businesses with high returns on Invested capital (ROIC) as the key driver of long-term returns for investors. Arista’s return on invested capital grew from 15% in 2018 to 29% in 2023. The average return on capital over the recent 5 years was 25.4% which is higher than Arista’s WACC (weighted average cost of capital) of 12.34%. This implies that the business continues to create value for its shareholders. The return on assets of Arista Network as of 9/30/2024 was 23.7%. Return on assets has been over 20% since the quarter ending 9/30/2022. For the full year 2023, the company generated $2.257 billion on $9.946 billion of assets or a 22% return on assets. This is an indication of how efficient the company generates profit from its capital.

High Operating Income Margin

For a manufacturer of networking equipment, Arista has increased its operating margins over time. Operating margins grew from 12.74% in 2018 to 42.12% as of the quarter ending 9/30/2024. Arista’s ability to grow its operating margin is reflective of its pricing power and operational efficiency. Companies with high operating margin are more likely able to withstand the stresses of economic challenging environments.

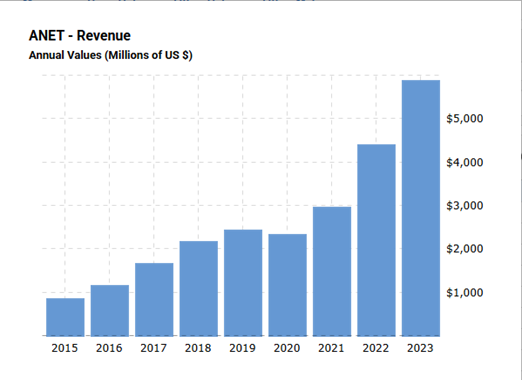

Revenue and Operating Income Growth

Revenue grew from $2.1 billion in 2018 to $5.9 billion in 2023. That is over a 180% increase in revenue over a 5-year period. If you look at a 10-year period, revenue grew from $361 million in 2013 to $5.9 billion in 2023 which is a 1,543% growth. Over the last 10 years, the company was able to grow its revenues at an annual rate of 32.1% per year.

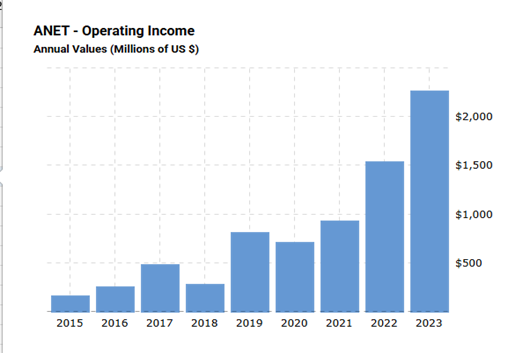

Arista was able to raise its operating income at a faster pace than its revenues which is an indication of operating efficiencies. Operating income grew from $273 million in 2018 to $2.3 billion in 2023 which is 726% growth. If you look at a 10-year period, operating income grew from $66 million in 2013 to $2.3 billion in 2023 which is a 3,319% growth rate.

Minimal Stock Buybacks

Arista has not been allocating its capital efficiently. Arista’s stock buybacks over the last 5 years have been minimal. Share outstanding has remained constant in the 1.2 billion to 1.3 billion shares. Most of the Arista’s operating cash flow has been accumulating as cash and cash equivalents. Over the last 5 years, cash and cash equivalents in the balance sheet grew from $2 billion in 2018 to $5 billion in 2023. For 2023, Arista had almost as much cash in its balance sheet as a full year’s revenue. In my opinion, this might not be the best way to allocate capital. If Arista cannot reinvest this capital in growth cap ex such as acquisitions, then perhaps it would be better returning the excess cash to the shareholders in form of stock buybacks.

Earnings Per Share Growth

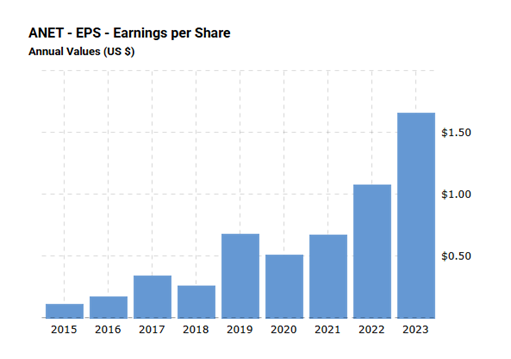

EPS has grown from 25 cents per share in 2018 to $2.08 per share as of Q3 of 2024 which is a 732% EPS cumulative growth in a little over a 5-year period. The average annual EPS growth over the last 5 years was 45.3% per year. Likewise, the stock price of Arista compounded an average of 49% per year over the last 5 years in line with the EPS growth rate of 45.3% per year over that same period. As Peter Lynch would say,

“If you can follow only one bit of data, follow the earnings—assuming the company in question has earnings. As you’ll see in this text, I subscribe to the crusty notion that sooner or later earnings make or break an investment in equities. What the stock price does today, tomorrow, or next week is only a distraction.” In Arista’s case, the stock price has compounded at a slightly higher rate than the EPS growth rate thus resulting to an over valuation over time. As far as future EPS growth, the average analyst EPS forecast for 2028 is $4.01 per share which reflects a 100% growth in EPS as compared to the most recent EPS of $2.08 in 2024. This represents a 100% EPS growth in a 4-year period. However, Analyst routinely change these estimates as new information comes out

Free Cash Flow Generation

A characteristic of a great company is its ability to generate substantial free cash flow, which can be reinvested or returned to shareholders. Arista’s free cash flow has grown from $947 million n 2020 to $3.178 billion in 2024. That is a 235% growth during that 5-year period. However, the stock price has outperformed the growth in free cash flow, growing 715% for the same time period. This indicates that the company might be overpriced since the stock price grew ahead of the company’s intrinsic value.

Strong Balance Sheet with debt at 50% or less of total assets: The company should have a solid financial position with minimal debt and ample liquidity.

ANET has a very strong balance sheet with total assets amounting to $9.946 billion as of 2023. Half of the assets or $5 billion consists of cash and cash equivalent. Total debt level amounted to $2.727 billion in 2023 which is approximately 27% of assets.

High Barriers to Entry: Significant barriers should exist to prevent new competitors from entering the market.

Arista’s high-speed switches and software-led approach as significantly differentiated from other networking competitors and very difficult to replicate. Arista’s strength in high-speed switching should generate economic profits for Arista in the decades to come. Arista’s networking switches for high-speed applications are best of breed resulting from a software-led approach over its networking hardware. Arista’s specialty within networking is high-speed switches, at speeds of 100 gigabits or more, that are designed for data centers. These switches create a local network to then connect to a wider network and the internet. Data traffic continues to explode increasing the need for Arista’s gear. Arista’s high-speed switches are the preferred option of both public cloud providers and enterprises building private clouds, and it occupies roughly one third of the market for 100-gigabit ports and faster. It has gained this share steadily since its founding in 2004 and has dethroned networking colossus Cisco at high speeds.

Arista’s extensible operating system, or EOS, sets it apart from Cisco and other networking players and represents considerable intangible assets which is reflected in its wide gross profit margins rivaled only by Cisco. EOS presents a unique value proposition. Arista’s decentralized and open structure makes it appealing to hyperscalers with large IT teams that want to fine-tune software for mass deployment, while its robust array of features and modular APIs makes it easy to deploy for smaller-scale enterprise data centers. For all customers, Arista’s single image and fault-containment offer the possibility of easier network upgrades and lower downtime. This contrasts with a networking competitor like Cisco, which focuses on features but locks customers into a closed ecosystem of chips, hardware, and software, all of which generate significant switching costs at their respective customers.

Excellent Management and Good Governance: The company should be led by a capable and ethical management team with strong corporate governance practices.

Regarding Arista’s management and corporate governance, Arista Networks has a leadership structure that blends seasoned industry veterans with a focus on engineering and innovation. Its key management is composed of it CEO and President Jayshree Ullal. Ullal is a networking industry veteran with extensive experience at Cisco, Ullal has led Arista since its founding in 2004. She’s highly regarded for her strategic vision and execution. The founder and Chief Technology Officer Kenneth Duda is a pioneer in networking software, Duda provides the technological foundation for Arista’s products. His deep technical expertise drives the company’s innovation. Ita Brennan (CFO) brings strong financial leadership to Arista, overseeing the company’s financial strategy and reporting. Anshul Sadana (Chief Operating Officer) is responsible for Arista’s global operations, including engineering, product management, and supply chain.

Arista’s board comprises experienced individuals from the technology and business sectors, providing independent oversight and guidance. The board has various committees, including audit, compensation, and nominating and corporate governance committees, that ensure responsible management and ethical practices. Arista maintains a one-share, one-vote structure, giving all shareholders an equal voice in company matters. The company is committed to transparent communication with investors through regular financial reporting, investor presentations, and an active investor relations program.

Arista’s management and governance structure emphasizes strong leadership, technological focus, financial discipline, and accountability. This structure has contributed to Arista’s success in the competitive networking market and its strong reputation among investors.

Limited Exposure to Extrinsic Risks: The company should be less susceptible to uncontrollable external factors that could negatively impact its performance. Arista’s sales are concentrated in the cloud networking market, which can exhibit cyclicality and lumpy spending patterns from customers. This lumpiness can be exacerbated by Arista’s concentration in customers like Microsoft and Meta Platforms. Softer spending patterns at these customers can cause top-line performance to suffer, as seen in 2019 and 2020 when Meta skipped an upgrade cycle.

Market Cap is above Intrinsic Value

Benjamin Grahm always emphasizes the importance of maintaining a margin of safety. This is done by not overpaying for a business even if it is a great business. Arista has a market cap of $143 billion as of January 30, 2025, trading at a P/E ratio of 55. Its average annual compounded revenue growth rate over the last 5 years was 22.2%. Based on this, a reasonable P/E should be approximately 37 in the conservative side. Arista’s intrinsic value based on its current net income should be around $100 billion. However, the revenue growth rate of Arista has accelerated in the recent 3 years to 36.2% per year. If you were going to use the more conservative estimate of its intrinsic value, Arista appears to be overpriced. There is no margin of safety if you were to initiate a position in today’s prices. It appears that its high growth rate is already priced in today’s market capitalization, and you may have to wait for its intrinsic value to grow into its market capitalization. In conclusion, Arista Networks appears to be a great company. Nonetheless, investing in the company at its current valuation may not provide investors with an adequate margin of safety. Further, having 40% of your revenue concentrated on just two customers poses a significant risk to the business.

Kenneth U. Reyes is founder and Managing Partner of Reyes Capital Management, LLC which manages a long term value oriented private investment fund. He is also founder of the Law Offices of Kenneth U. Reyes, APC, a five lawyer boutique law firm in Los Angeles specializing in Family Law. He can be reached at (213) 500-4836. [email protected]. 3699 Wilshire Blvd., Suite 747, Los Angeles, CA 90010.